When Money Problems Aren't Really About Money: A Conversation with Rick Kahler

I've been thinking a lot about resilience lately.

Not the motivational poster kind. The real kind. The kind you need when your body stops cooperating, when everything you thought was solid turns out to be remarkably fragile.

And here's what keeps surprising me: money sits right at the center of almost every resilience challenge I'm facing.

Which is weird, right? I'm 73 years old. I've worked in finance for decades. I should have the money thing figured out by now.

Except I don't. Not really.

When I got diagnosed with two aggressive cancers simultaneously, my first thought wasn't about survival rates or treatment options. It was about money. Would I drain my savings? What would happen to Suzanne if I died?

These questions kept me up more than the cancer did some nights.

That's when I started digging into financial therapy. And that's how I ended up talking with Rick Kahler, one of the pioneers who helped create this entire field back around 2008-2009.

The Thing Nobody Tells You About Financial Decisions

Rick told me something early in our conversation that I'm still processing.

"About 95% of financial decisions are emotional, not logical."

I wanted to argue with him. I've spent years working with numbers, with what I thought was rational decision-making.

But he's right.

Think about the last time you made a big financial choice. Maybe you bought something expensive you couldn't really afford. Or you avoided looking at your retirement accounts for months because it felt too scary.

The math isn't the hard part. Any decent calculator can tell you what you should do with your money.

The hard part? Understanding why you do what you actually do.

"I see clients all the time who earn six figures but are always broke," Rick said. "And I see people who make modest incomes but somehow feel financially secure. The difference isn't the numbers. It's what's happening underneath."

That "underneath" part is where financial therapy lives.

What Financial Therapy Actually Is

Financial therapy sits at the intersection of money and emotions. It's not traditional talk therapy. It's also not standard financial planning.

It's something distinct that blends both.

A regular financial planner will show you a budget. They'll tell you that you can't spend more than you earn. They'll focus on the math, which is completely sound.

Problem solved? Not really.

"About 80% of money problems don't fix with logic alone," Rick told me. "They come from past events, family teachings, old emotional hurts. Your overspending might trace back to how your parents managed money when you were a kid."

This hit me hard.

I grew up watching my father use money as a weapon. If we did what he wanted, we were "rewarded" with things we actually needed—not luxuries, just basic stuff. If we didn't comply, he'd threaten to withhold money.

It was control disguised as parenting.

And you know what I did? I rebelled in the opposite direction. My money script became: "I will never use money to control people. I will never make people jump through hoops for what they need."

Sounds noble, right? Except that script has caused me problems my entire adult life. I give money away too easily. I don't set healthy boundaries. I feel guilty asking for anything in return.

These patterns live in your subconscious. They drive your actions without your awareness.

Rick calls them "money scripts." And everyone has them.

The Parts of You That Fight About Money

One of the approaches Rick talked about is something called Internal Family Systems, or IFS.

The basic idea is that we all have different parts of ourselves. You know this feeling already. We all have inner conflicts.

I told Rick about my own struggle. One part of me wants to be incredibly generous, to give money away to causes I care about. Another part is terrified about running out of resources, especially now that I'm facing ongoing cancer treatment.

These parts are constantly fighting. And I'm caught in the middle.

"Every part of you has a good intent," Rick explained. "Even the parts that seem to hurt your financial security are trying to help you in some way."

Your part that overspends might be trying to help you feel valued or loved. Your part that hoards money might be desperately trying to keep you safe from poverty.

Rick told me about a client who had two parts in sharp disagreement. One wanted to donate everything to charity. The other wanted to save every penny out of fear.

"We helped each part tell its story," he said. "The giving part explained its love for helping others. The saving part shared its worries about becoming destitute. Neither part was wrong."

This is where it gets interesting.

"Once both parts felt genuinely heard, they began to work together. The saving part made a promise. It said if they could save enough for a strong emergency fund, they could give away the rest. Suddenly, both parts won."

I'm working with my own IFS therapist on this same approach. It's slow work. Some weeks, I make progress. Other weeks, those parts are just screaming at each other, and I feel stuck.

But I'm starting to understand that these aren't random impulses. They're actual parts of me trying to protect me based on what they learned when I was young.

My generous part is still rebelling against my father's control. My scared part remembers what it felt like to have money used as a weapon and never wants to be vulnerable like that again.

Both parts are trying to help. They just have different strategies.

The Trauma Piece Nobody Talks About

Most ongoing money problems stem from financial trauma.

And no, this doesn't always mean major, tragic events.

"There's 'big T' trauma like abuse or profound loss," Rick said. "But there's also 'little t' trauma. The many small hurts that accumulate over time."

Maybe your parents argued about money when you were little. Maybe you watched your family lose everything during a downturn. Maybe, like me, you had a parent who used money to manipulate and control.

These experiences wire your brain for self-protection. Those patterns made perfect sense at the time.

But now they might create more problems than they solve.

I think about my own cancer journey. The first time I had cancer, fifteen years ago, I went into pure survival mode financially. I cut back on everything. I hoarded cash.

It made sense then. I was scared.

But I carried those patterns forward for years afterward, long past when they were useful. My brain had learned that uncertainty equals danger equals save everything.

Now I'm facing cancer again. And my brain wants to do the same thing—retreat, hoard, protect.

Except this time I'm trying to understand what's actually happening. Why do I react this way? What is this protective part of me trying to accomplish?

"Financial therapy offers a safe place to work through these old wounds," Rick told me. "You start to understand where your unique money scripts come from. You can update beliefs that no longer serve you."

Money Scripts: The Invisible Beliefs Running Your Life

Rick asked me to think about the phrases that run through my head about money.

Things like: "Money is the root of all evil." "Rich people are greedy." "I'll never have enough." "More money will solve everything."

These scripts run quietly in your mind's background. Most were passed down from your family.

I realized I carry a script that says: "Money should never be used to control people."

This explains so much about my financial behavior. I give too freely. I don't enforce boundaries. I feel guilty when I have more than others.

It's all a reaction to my father's control.

"Financial therapy helps you find your specific money scripts," Rick said. "Then you can see if they're true or helpful. You get to challenge them."

Some scripts need a complete rewrite. Others just need slight updates to fit your current life.

Mine needs updating. I'm learning that setting financial boundaries isn't the same as using money to control people. I can say no without becoming my father.

I'm working on it.

Building Resilience Around Money

Here's what I'm learning about resilience and money.

Real resilience isn't about toughness or positive thinking. It's about flexibility. It's about adapting to new realities instead of rigidly insisting things should be different.

My cancer diagnosis forced me to face some uncomfortable financial truths.

I might not live to 80. Maybe not even 75. So what am I saving for? Should I be spending more now? Should I give money away while I can still see the impact?

These aren't spreadsheet questions. They're questions about what actually matters.

Rick helped me understand that financial resilience comes from understanding your scripts and your parts.

"When you know why you react the way you do, you have choices," he told me. "Before that, you're just running on autopilot, repeating the same patterns."

My saving part isn't wrong. It's trying to keep me safe. But it's using outdated information from past scares and old family dynamics.

I'm trying to let that part know we're okay now. We have enough. We can loosen the grip a little.

Some days this works. Other days that part takes over completely and I'm back to checking my bank balance three times a day.

But I'm noticing the pattern now. That's progress.

The resilient people aren't the ones who never struggle with money. They're the ones who understand their struggles and can work with them instead of against them.

The "It Is What It Is" Philosophy Applied to Money

I say "it is what it is" a lot.

People think it sounds defeatist. But it's not.

It means accepting reality as it actually exists, not as you wish it were.

I have cancer. It is what it is.

My father used money to control us. It is what it is.

That last one took me years to accept. I wanted him to have been different. I spent decades angry about it.

But Rick helped me see that acceptance isn't approval.

"Once you accept what actually is, you can start working with reality instead of fighting it," he said.

The exhausting part isn't the reality itself. The exhausting part is the constant internal argument: This shouldn't have happened. This isn't fair. Why me?

Those thoughts don't change anything. They just drain your energy.

Financial resilience comes from accepting what is and then asking: "Given what is, what now?"

I can't change my father or my childhood. But I can change how those experiences continue to affect my current relationship with money.

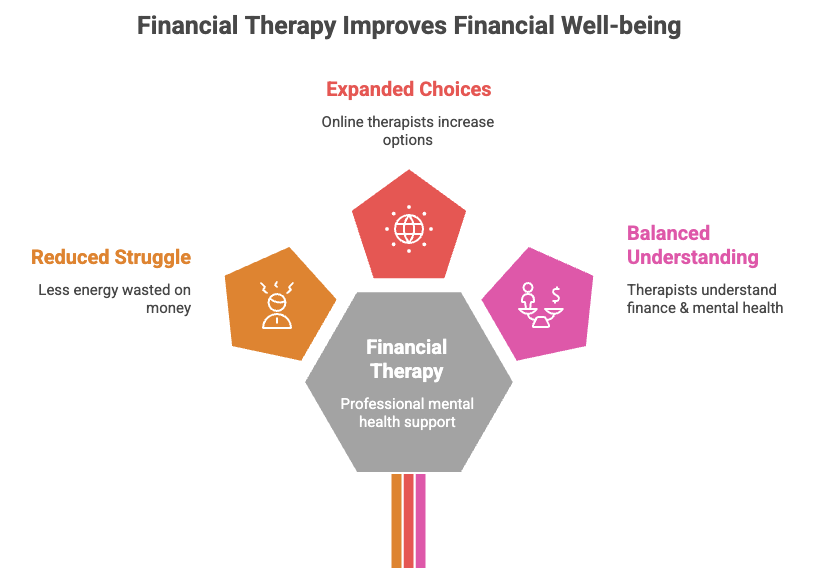

Finding Help: Where to Start

If you're thinking about financial therapy, here's what Rick told me about finding someone qualified.

Look for someone with a certified financial therapist designation. This usually comes from the Financial Therapy Association, which Rick helped establish back in 2009.

The Association has an online directory where you can search for practitioners. Don't be surprised if there aren't many options near you. It's still a growing field.

But here's the good news: many financial therapists now work online. This expands your choices significantly.

Rick suggested asking potential therapists about their background. Do they have training in both finance and mental health? The key is that they understand both sides.

Also, ask about their approach. Some focus on behavioral methods. Others, like Rick, use IFS extensively. The method should feel right for you.

Sessions typically cost between $150 and $300 per hour. Some therapists offer sliding scale fees based on income.

"I know it's not cheap," Rick said. "But ask yourself what it's costing you to keep struggling with the same patterns year after year."

That hit home for me. I've wasted so much energy fighting with myself about money.

You can find the Financial Therapy Association's directory on their website. Just search for "Financial Therapy Association," and you'll find it.

Where This Leaves Me

Financial therapy gave me something I never expected.

It helped me see that my money problems were never really about money. They were about my father's control, about rebellion, about old family patterns and unhealed wounds.

When you understand where your money scripts come from, everything starts to shift.

You stop fighting with yourself. You start working with your different parts instead of against them.

I'm 73 years old. I'm facing cancer. My body's making decisions without my permission.

But I'm learning something crucial: resilience isn't about controlling outcomes. It's about adapting with flexibility instead of breaking with rigidity.

My father used money to control. I rebelled by refusing to set any boundaries with money. Both approaches were rigid. Both caused problems.

Now I'm learning flexibility. Sometimes I give freely because it aligns with my values. Sometimes I set boundaries because that's healthy. I get to choose based on the actual situation, not just react based on old scripts.

That's resilience. That's what Rick helped me start to understand.

If you've tried everything else and nothing has stuck, maybe it's time to look deeper. Maybe it's time to explore the emotional side of your finances.

Financial therapy might be the missing piece.

It was for me.

And I'm genuinely curious: what money scripts are running your life? What old family patterns are you still acting out?

Let's figure this out together.

Facebook

LinkedIn

Youtube