When Money Problems Aren't Really About Money

I've been thinking a lot about money lately.

Not in the way I used to think about it when I was running businesses or managing other people's wealth. That was all spreadsheets and projections and market analysis. That felt safe. Controllable.

This is different.

I'm 73 now. I've got two cancers. My relationship with money has shifted in ways I didn't expect. And honestly? I'm not sure I ever really understood what was driving my money decisions in the first place.

So when I had the chance to talk with Rick Kahler, one of the pioneers of something called "financial therapy," I jumped at it. Rick's a CFP with a master's degree and multiple certifications, but he's spent the last couple of decades focused on something most financial advisors completely ignore: the emotional side of money.

Here's what we figured out together.

The Thing Nobody Tells You About Financial Planning

"Let me paint you a picture," Rick said early in our conversation. "Someone comes to see a traditional financial planner. They're spending more than they earn every month. The planner shows them a budget. Says they need to spend less than they make. Problem solved, right?"

And I get it. The math is simple. Don't spend more than you earn. Anyone can understand that.

"Except it doesn't work," Rick continued. "Because about 80% of money problems aren't actually about the math. They're about something else entirely."

This hit me hard. I spent years as a wealth manager. I built businesses. I taught people about money. And yeah, I focused almost entirely on the numbers.

But here's the thing I'm learning now: the numbers are the easy part.

Rick told me about research showing that up to 95% of our financial decisions are emotional, not logical. We like to think we're rational about money. We tell ourselves stories about why we made this purchase or that investment. But most of the time? We're rationalizing decisions we already made based on feelings we don't fully understand.

"Your overspending might trace back to how your parents handled money when you were a kid," Rick explained. "Or fear from a time you didn't have enough. These past moments shape your current relationship with money more than any spreadsheet ever will."

I sat with that for a while. Started thinking about my own childhood. My parents' relationship with money. The messages I absorbed without even knowing it.

The Money Lessons I Learned Young

Rick's comment about parents and money hit harder than I expected.

My father used money as a weapon. That's the truth of it.

Love in our family came with a price tag. Literally. Whether he'd pay for something - college tuition, help with a car, support during a rough patch - depended entirely on whether we were behaving the way he wanted.

If you were in his good graces, the checkbook opened. If you weren't, it slammed shut.

I remember watching him do this with my niece. The constant calculation in our heads: "If I do this, will he still pay for school? If I say that, will he cut me off?" Money wasn't just money in our house. It was approval. It was control. It was the measure of whether you were worthy of love.

And here's the thing - I didn't realize until talking with Rick how much that shaped everything I did with money later.

But not in the way you might think.

I didn't become my father. I rebelled against him. Hard.

I swore I would never use money as a club the way he did. I would never make people jump through hoops for my approval. I would never measure out love based on money.

I was so determined not to be my father that I became just as dysfunctional in the other direction. He used money to control. I thought I used it to prove I wasn't controlling. Both of us were using money for something other than what it actually was.

And here's what really gets me: I thought I was different. I thought I'd escaped his pattern. But I was still letting him control my behavior. Just from the opposite angle.

I was still making decisions based on him. Still reacting to him. Still letting that childhood dynamic run my adult financial life.

What money scripts am I still running that I learned at that dinner table 60 years ago? And how many of my "generous" financial decisions were actually about healing something broken in me rather than genuinely helping someone else?

Those are hard questions to sit with.

What Financial Therapy Actually Is

So what is financial therapy? I asked Rick to break it down.

"It sits right at the intersection of money and emotions," he said. "It's not traditional talk therapy. It's not standard financial planning. It's a distinct field that blends financial knowledge with emotional support."

The field really took off around 2008 and 2009. That's when experts like Rick started realizing that money and feelings were completely intertwined. You couldn't separate them, even though most professionals were trying to.

Financial planners handled the numbers. Therapists handled the emotions. But nobody was working in the middle ground where most people actually live.

Rick helped found the Financial Therapy Association in 2009 to change that. To create a space where professionals could address both sides of the money equation.

"We needed a field that understood both the mechanics of money and the psychology of money," Rick explained. "Because you can't fix one without addressing the other."

Here's how Rick explained the difference:

A financial planner asks: "What should you do with your money?"

A financial therapist asks: "Why do you do what you do with your money?"

Both questions matter. But that second one? That's the one most of us have never really explored.

I know I haven't. Not deeply. And I'm supposed to be someone who knows about this stuff.

The number of certified financial therapists is still small across the country. While the field's growing, finding someone with this specialty remains challenging. There's high demand, but supply hasn't caught up.

Rick mentioned that most financial professionals handle numbers and investments. Mental health experts focus on emotions and behaviors. But historically, very few worked in this vital middle ground.

And that's the problem. Because our money lives exist entirely in that middle ground.

The Parts of You That Fight About Money

Rick introduced me to something called Internal Family Systems, or IFS. At first, it sounded a bit odd. But the more he explained it, the more it made sense.

The basic idea: we all have different parts of ourselves. You've felt this. We all have.

One part of you wants to save for retirement. Another part wants to take that big vacation now. One part feels guilty spending on yourself. Another part resents always giving to others.

These aren't just random thoughts. They're actual subpersonalities within you. Each one has its own voice, its own fears, its own hopes.

Rick told me about a client who had two parts in sharp disagreement. One part wanted to donate everything to charity. Felt tremendous responsibility to give back. Felt shame about keeping money for himself.

The other part was terrified about the future. Wanted to save every penny. Feared ending up broke and helpless.

These two parts were at war. The client was stuck in the middle, completely paralyzed. Couldn't make any financial decisions at all.

"The therapist helped each part tell its story," Rick explained. "The giving part got to explain its love for helping kids. Its passion for doing good. The saving part shared its worries about becoming destitute. Neither part was wrong. They just had different concerns."

Here's where it gets interesting. Once both parts felt genuinely heard, they began to work together.

The saving part made a promise: if they could build a strong emergency fund, they could give away the rest. The giving part loved this. Suddenly saving money excited it, because more savings meant more future giving.

"Here's what's important," Rick said. "Every part of you has a good intent. Even the parts that seem destructive are trying to help you somehow."

The part that overspends might be trying to help you feel valued. The part that hoards money might be desperately trying to keep you safe.

The part that gives money away without thinking might be trying to prove you're not your father.

Both parts won. The inner conflict ended.

I'm still sitting with this. Thinking about my own parts. The part that wants to be generous. The part that's afraid of running out. The part that thinks I should have done better. The part that's tired of thinking about money at all.

The part that still wants to prove to my dead father that I'm nothing like him. The part that's still trying to make up for his withholding by over-giving.

What would happen if I actually listened to all of them?

The Trauma Piece Nobody Mentions

Rick said something that really landed: "Most ongoing problematic money behaviors stem from underlying financial trauma."

Now, when most people hear "trauma," they think of major events. Abuse. Profound loss. Big stuff.

But Rick explained there's also what therapists call "little t" trauma. The small hurts that accumulate over time.

"Maybe your parents fought about money constantly," Rick said. "Maybe you watched your family lose everything in a downturn. Maybe a teacher shamed you for not having lunch money. Maybe a parent used money to control you."

That last one. Yeah.

These experiences wire your brain for self-protection. Those patterns made perfect sense at the time. They helped you survive.

"But now," Rick said, "those old protective patterns might create more problems than they solve."

I thought about my own history. Times when money felt scarce. Decisions I made out of fear. The way I sometimes hoarded or sometimes spent without thinking.

The way I sometimes measured my worth - and other people's worth - by their relationship to money.

The way I'd give money away to prove something, without stopping to think about whether it was actually helpful. Or sustainable. Or even what I really wanted to do.

Financial therapy offers a safe place to work through those old wounds. To understand where your specific money scripts come from. To update beliefs that no longer serve you.

This isn't quick work. Rick was honest about that. It takes time. It can feel hard.

But it's the clearest path to making changes that actually last. To stopping the cycle of passing those patterns down to the next generation.

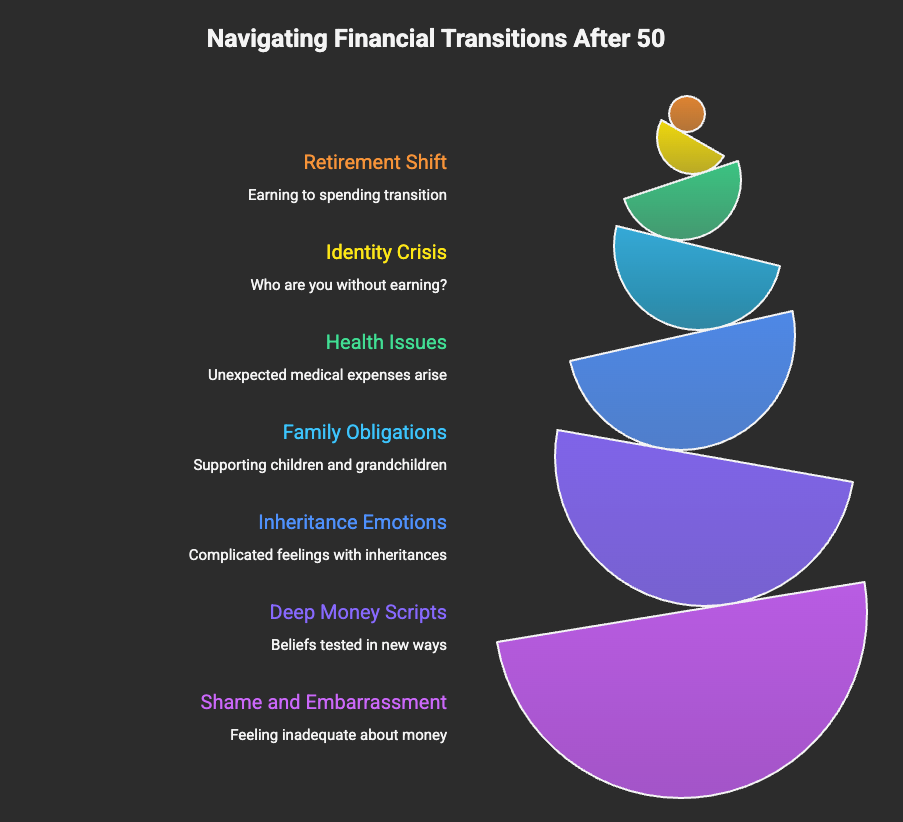

Why People Over 50 Need This Differently

I asked Rick specifically about people in my age group. People over 50 who've spent decades running certain money patterns.

"There's something unique that happens around this age," Rick said. "You've had more time to accumulate both wealth and emotional baggage around money. And you're facing transitions that force you to confront your relationship with money in new ways."

Retirement is the obvious one. The shift from earning to spending. From building to drawing down. That's not just a math problem.

"Who are you when you're not earning anymore?" Rick asked. "If your identity has been tied to providing, to building wealth, to being successful - what happens when that changes?"

And I get it. I'm living this right now.

But there's more. Health issues often show up in this decade. Parents die, often leaving inheritances that come with complicated emotions. Kids might need financial help in ways you didn't expect. Grandkids arrive.

"All of these transitions stir up your deepest money scripts," Rick explained. "The beliefs you've carried for 50, 60, 70 years suddenly get tested in ways they never were before."

For me, it's the cancer. Knowing my timeline is shorter than I thought. Suddenly, the question isn't "Do I have enough to last?" It's "What do I actually want this money to do in the time I have left?"

That's not a spreadsheet question. That's an emotional question. A values question. A "what really matters" question.

And I don't know that I have good answers yet.

Rick mentioned that people over 50 often carry tremendous shame about not having their money figured out by now. "You think you should have this handled. You're embarrassed to admit you're still struggling with money at 60 or 70."

But here's what Rick said that helped: "The people who struggle most with money aren't stupid. They're often very successful in other areas. The struggle isn't about intelligence. It's about unresolved emotional patterns."

That lands differently than being told to just budget better.

When This Might Matter for You

I asked Rick when someone should consider financial therapy instead of just traditional financial planning.

"If money creates ongoing stress in your life, that's a sign," he said. "Frequent arguments with your partner about finances. Hiding purchases or having secret accounts. Earning good income but always being short on cash. Or having plenty saved but being terrified to spend any of it."

These extremes usually mean something emotional is running the show.

Rick mentioned that people going through major life changes often benefit greatly. Retirement, for example, causes more than just a financial shift.

"The change from saving money to using it is harder than it seems," he explained. "It's not just about having enough. It's about identity. Who are you when you're not earning anymore?"

This one hit close to home. I'm navigating my own transition right now. Stepping back from active business. Facing health challenges that have shortened my timeline. Wondering what matters most when time feels limited.

And yeah, money feels different now. Not because the numbers have changed. Because I have.

Divorce, inheritance, selling a business - these events stir up feelings you don't expect. They make you face your true relationship with money in ways spreadsheets never will.

"If you grew up with money worries," Rick added, "financial therapy can help break those cycles. You don't have to pass those patterns on to your kids."

That matters to me. I don't want my children or grandchildren carrying money anxiety I never dealt with. I don't want them measuring love by the checkbook the way I learned to.

I don't want them using money as a weapon the way my father did. Or swinging to the opposite extreme the way I did, giving without boundaries just to prove they're different.

The Questions I'm Left With

Here's what I'm sitting with after talking to Rick:

What money scripts am I running that I learned as a kid? Which ones still serve me, and which ones don't?

How much of my relationship with money is actually about my father? About proving something to him even though he's been dead for years? About being the opposite of him, which is still being controlled by him?

What are my different parts trying to protect me from? And are they still protecting me from real threats, or from things that happened 50 years ago?

How much of my financial stress is actually about money, and how much is about something else entirely - control, love, worth, identity?

If I only have a decade left - maybe less - what do I actually want money to do for me? What does it mean to spend down rather than build up? How do I shift from accumulation to distribution without feeling like I'm losing control or security?

When I give money to someone, am I actually helping them? Or am I trying to heal something in myself? How do I tell the difference?

These aren't questions with simple answers. And I get it - that's uncomfortable. We want certainty. We want someone to tell us the right answer.

But maybe that's the whole problem. Maybe we've been looking for financial answers to emotional questions.

Why This Matters Now

Rick said something toward the end of our conversation that I keep coming back to: "The older model of only logical financial advice isn't enough anymore. We need approaches that address the whole person. Both the numbers and the feelings."

I've spent my whole career on the numbers side. I'm good at that part. I can read a balance sheet. I can build a budget. I can project returns and manage risk.

But the feelings part? That's newer territory for me. And I'm starting to think it might be more important than all the spreadsheets I've ever created.

Financial therapy isn't about replacing good financial planning. You still need to understand the math. You still need sound strategy.

But if you keep making the same money mistakes over and over despite knowing better? If money causes more stress than it solves? If you've got plenty but still feel anxious all the time?

If you find yourself using money the way your parents did, even though you swore you never would? Or if you're using it in the exact opposite way, which might be just as dysfunctional?

Maybe it's time to look at the emotional side. Maybe it's time to ask different questions.

What I'm Going to Do

I'm not sure yet if financial therapy is something I need. But I'm curious about it now in a way I wasn't before talking to Rick.

I'm going to start paying attention to my money patterns differently. Not just tracking spending, but noticing how I feel when I spend. What triggers anxiety. What brings relief. What parts of me are fighting about money decisions.

I'm going to sit with the question of my father. How much of my money behavior is still about him. Still reacting to him. Still trying to prove something to him. How much of my generosity is actually generous, and how much is just rebellion dressed up as virtue.

Here's what I'm learning at 73: the goal isn't to have it all figured out. The goal is to keep being curious. To keep exploring. To stay open to the possibility that there are better ways to think about things I assumed I already understood.

Maybe you're curious about this too. Maybe you've wondered why you do what you do with money. Maybe you're tired of the same patterns showing up over and over.

Maybe you learned something about money from your parents that's still running your life. Maybe you're using money in ways you swore you never would. Or maybe you're doing the opposite of what your parents did, and it's still not working.

I don't have answers for you. I'm still figuring this out myself.

But I'm starting to think that asking better questions about the emotional side of money might be more valuable than having all the logical answers about the financial side.

What do you think? Have you ever wondered why you do what you do with money? What patterns show up for you that you can't quite explain? What did you learn about money as a kid that you're still carrying? Are you rebelling against those patterns, or repeating them, or some weird combination of both?

I'd genuinely love to know. Because we're all figuring this out together.

It is what it is. But maybe understanding the "why" behind our money behaviors gives us more choice about what comes next.

If you want to learn more about financial therapy, you can check out the Financial Therapy Association or explore Rick Kahler's work. And if this resonated with you, I'd love to hear your thoughts in the comments.

Facebook

LinkedIn

Youtube